Catastrophic climate change, cybercrimes, and shifting financial market volatility are prompting insurers to reconsider how they engage with prospective clients. Instead of focusing solely on post-incident payouts, forward-thinking insurers are investing in strategies that help clients reduce risk and prevent insured events before they occur. Software development teams create AI-driven risk assessment tools to support proactive management and deliver positive outcomes for clients and businesses.

We aim to demonstrate how insurance innovations improve operational cost efficiency, cyber resilience, and the customer experience. What to expect in the insurance industry and how to identify emerging opportunities for startups and large companies to introduce innovative products to market. These solutions set their offerings apart and attract customers through meaningful, technology-driven value. This involves using advanced technologies (AI, IoT, cloud, data analytics, etc.) and customer-focused digital channels to meet rapidly changing expectations.

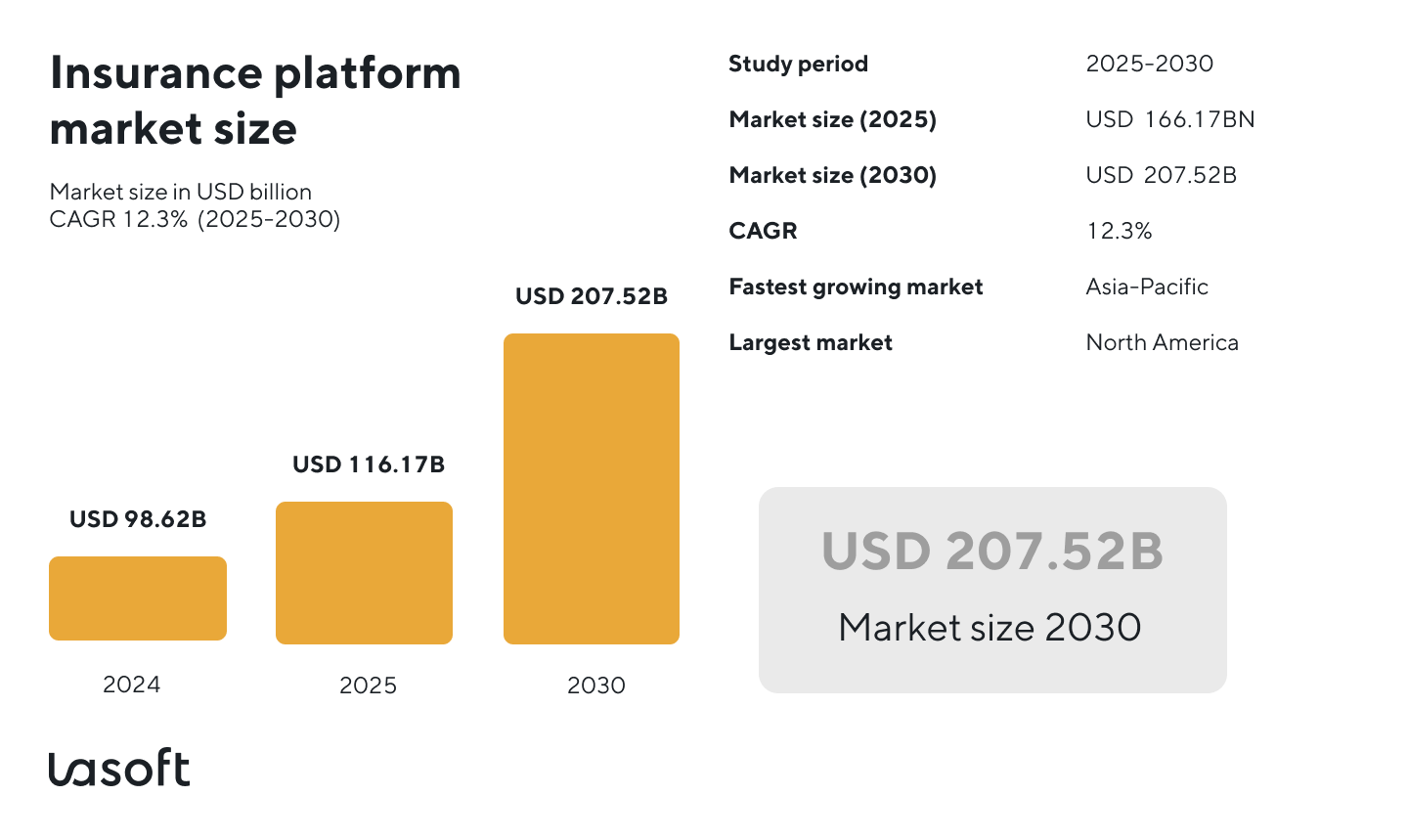

Insurance Sector Growth Drives Insurance Platform Market

The insurance platform market is projected to reach USD 116.16 billion by 2025 and USD 207.52 billion by 2030, with an annual growth rate of 12.3%. Many B2B SaaS companies are embracing this trend, creating user-friendly, streamlined solutions that include payment processing, risk management, automated underwriting, and claims processing.

Source: Marketsandmarkets

Digital Insurance Market Trends

Today’s insurance customers expect human-like interactions (a challenging task in the AI era), hyper-personalization, and instant service, all available 24/7. In the digital market, agile insurtech start-ups and tech-savvy teams pose a fierce competitive threat. To stand a chance of keeping up, you need to be aware of the key tech trends driving the insurtech revolution:

Artificial Intelligence and Machine Learning

Artificial Intelligence (AI) is increasingly integrated into insurance workflows, supporting underwriting, claims processing, and personalized customer service that closely mirrors human interactions. To fully utilize the vast amount of data, including job history, previous claims, social media content, and local weather conditions, you require a highly skilled individual who can effectively integrate this data into generative AI and ML models. This lets you run the numbers and dig deep to determine a customer’s risk profile and craft a pricing model to match.

Meanwhile, the best insurtech companies are deploying AI-powered chatbots and virtual assistants to handle quotes and answer customer queries, resulting in highly personalized interactions that get customers on board and engaged. In the claims department, AI can significantly help by automating triage and, more importantly, identifying suspicious claims.

Data Analytics and Big Data

Many businesses and insurers are developing analytics software, including dashboards, predictive models, and real-time reporting, to support decision-making. Advanced analytics enable personalized recommendations, dynamic pricing, and better risk assessment. For example, predictive models can flag fraudulent claims with 30–40% higher accuracy. Telematics and IoT devices (in cars, homes, and wearables) generate continuous data streams, enabling insurers to price and manage policies based on actual usage.

Cloud Computing

Cloud Computing

Cloud adoption is enabling insurers to scale systems quickly, integrate partners, and launch digital services. Cloud-based policy administration and claims systems offer enhanced scalability and retain clients, encouraging them to buy new products. As software development experts, we provide secure cloud migration. We are open to our clients and always advise them to follow our practices. Migrating legacy systems to a reliable, cost-effective cloud platform reduces server infrastructure costs and provides agility, enabling insurers to rapidly spin up new digital applications. Review our comparison of AWS, Google Cloud, and Hetzner Cloud to understand why we moved our projects to Hetzner. At Lasoft, transitioning our internal projects from AWS to Hetzner has significantly improved cost efficiency and infrastructure control. We believe many companies, especially small- to mid-sized ones or those operating in Europe, can achieve similar benefits and improved resource utilization.

Internet of Things

IoTs deliver value through data collection. Devices such as vehicle telematics, smart home sensors, health-tracking wearables, and industrial IoT systems for commercial buildings help insurers gain insight into how their customers behave and what threats may exist in their environments.

The changes they now offer shift from simply reviewing historical data to obtaining real-time incident information. For instance, auto insurers can now offer premiums based on driving behavior because they have telematics data to support it, meaning safe drivers receive lower premiums.

Smart sensors in property insurance can detect water leaks, fires, or break-ins and alert everyone immediately, helping prevent significant damage.

Wearable health devices are providing a constant stream of health data that life and health insurers can use to nudge their customers towards healthier lifestyles and even tailor underwriting to each individual.

When insurers want to stay ahead in a market that opens transformative opportunities, they use emerging technologies to gain an edge.

Blockchain

As a decentralized database system, blockchain provides secure signing, exchanging, and verification of transactions and records without a central authority. Blockchain technology has the potential to significantly disrupt legacy systems in the insurance sector. The potential of this solution to enhance transparency and security makes it highly appealing for use across many insurance operations. Blockchain technology streamlines claims processing by creating a secure, immutable record of transactions, reducing the risk of fraud and administrative errors.

In addition, blockchain-enabled smart contracts can automate policy execution and claim settlements, resulting in more reliable outcomes. Traditional insurance companies are actively investigating blockchain technology to develop innovative business models and enhance operational efficiency, positioning them as industry leaders.

Established insurance companies, innovative tech entrepreneurs (startups), and large digital corporations are the key participants in the blockchain insurance industry. Blockchain insurance covers property and casualty, life and health, and reinsurance. Blockchain technology has been developed in both established and emerging areas and has been deployed across public, consortium, and private blockchains.

Sustainability and Green Insurance

As environmental threats intensify, ESG (Environmental, Social, and Governance) standards encourage a more sustainable, mindful approach to living. Insurance companies are driving much of the change toward a low-carbon economy and greener practices, prompting a rethink of how they underwrite, invest, and design their products.

1. Dealing with Climate Risk

Insurers are turning to new technologies, such as the Internet of Things, Artificial Intelligence, and geospatial analysis, to develop climate risk models that incorporate satellite data, environmental simulations, and long-term performance metrics.

2. Encouraging People to Live More Sustainably

Insurance companies are starting to offer products that encourage people to make more eco-friendly choices

Green property insurance gives discounts or better terms for homes that use energy-efficient building materials, have solar panels installed, or are built using sustainable construction materials.

Eco-friendly car insurance that rewards people for driving electric vehicles or keeping low mileage.

Special insurance is available to cover new renewable energy projects, such as wind farms, solar panels, or solar desalination systems, particularly when traditional methods are ineffective.

3. Bringing ESG into the Mainstream

Many insurers are now incorporating ESG standards into their practices, declining to insure projects that harm the environment and requiring their business clients to disclose their sustainability performance. On the investment side, insurers are allocating capital to green bonds, clean energy, and climate innovation funds.

Embedded and On-Demand Insurance

Embedded insurance means coverage integrated directly into digital platforms that offer other services, such as healthcare websites, travel booking apps, fintech services, or automotive marketplaces.

Such features create new distribution channels that leverage API integration and a seamless UX, helping users see the benefits of choosing additional services.

On-demand insurance lets customers activate coverage anytime and meets the expectations of modern users with fast-paced lifestyles, with digital identity verification and fraud protection.

Transforming Customer Engagement

AI-powered chatbots and virtual assistants are also enhancing engagement. They provide instant responses to customer queries, generate quotes, and send personalized renewal reminders. Chatbots can segment customers by behavior and risk profile to push relevant products or send alerts. For example, AI assistants may analyze customer data to recommend questionnaires for their life policies or detect when a car owner could benefit from switching to another plan. In trials, insurers using AI personalization have seen notable increases in retention and engagement as customers receive more relevant service.

Case Studies and Outcomes

We offer real-world examples that illustrate the tangible impact of insurance innovation on the startup’s success.

Building a Cyber Insurance Platform with Emerging Tech

We offer an example of Lasoft’s collaboration with Zala to build a specialized cyber insurance platform for small and medium-sized businesses (SMBs) in the United States.

With the rising frequency of cyber threats, demand for SMB-focused cyber insurance has surged. However, most legacy insurers can’t address this risk, so a US startup came up with the idea of developing a flexible platform that could:

- Offer unique coverage for SMBs based on their cyber risk profiles.

- Automate complex underwriting using up-to-date digital threat data.

- Streamline broker workflows for quoting, binding, and document generation.

- Ensure compliance with evolving regulatory and data security standards.

Custom Platform Development for an NY Insurance Company

A New York-based insurance company specializing in mergers and acquisitions (M&A) and commercial policies was struggling with legacy systems and useless functionality. Their manual workflows and legacy tools were limiting operational speed and scalability.

They contacted our experts at LaSoft with a clear mission: build a custom insurance management platform that would digitize business processes, centralize policy data, and enhance broker performance.

The client required an enterprise-grade solution with the following functionality:

- Supporting broker operations: quote creation, risk assessment, policy issuance, and renewal.

- Replacing manual document handling with automation and secure storage.

- Integrating internal data models with intuitive UI for non-technical users.

- Ensuring compliance with U.S. insurance regulations and data privacy laws.

Final Recap

The insurance industry is seeking solutions to meet customer expectations and mitigate external risks. Insurers who proactively adopt emerging technologies gain a significant competitive edge:

- Operational efficiency and automation across underwriting, claims, and customer engagement.

- Data-driven insights while using analytics dashboard solutions that lead to smarter pricing, personalized coverage plans, and fraud prevention.

- New business models and channels, including flexible products and seamless embedded offerings.

- Sustainability and ESG integration that align with global regulatory and stakeholder expectations.

To stay relevant and grow in a digital-first market, you must embed innovation at every level. At LaSoft, we specialize in translating ambitious insurance ideas into secure, scalable, and user-friendly digital platforms.